++

Why this matters

When you sell virtual currency, battle passes, or anything else directly to your players, two kinds of partners can move money from the player to your bank account:

Payment Service Providers (PSPs): Routes card and alternative payments to acquirers, tokenizes data, settles funds, while you remain the legal merchant responsible for calculating and remitting taxes, maintaining compliance, handling chargebacks, fraud liability, and issuing customer invoices.

Merchants of Record (MoRs): Becomes the legal seller, processes payments via its own PSP stack, collects and remits taxes, issues receipts, manages fraud and chargebacks, maintains compliance, and remits net revenue to you after an agreed fee.

Below is a concise, practical breakdown to help your team decide which is best for your business.

PSP vs. MoR pricing

When you think of payment costs, think in two buckets:

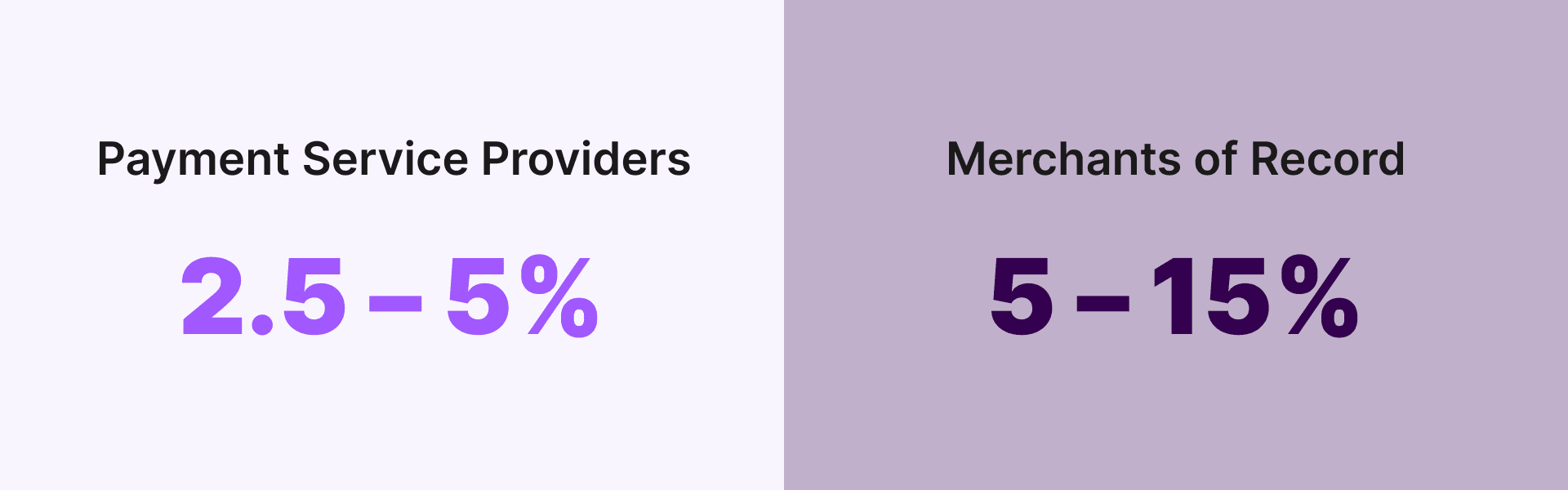

PSP costs

Average all-in cost: 2.5 – 5%

Processing fee: roughly 1 – 3% of the purchase price + $0.10 – $0.35 per transaction.

Extras that stack on top: cross-border FX (+1%), currency conversion (+1.5%), extra costs for alternative methods like carrier billing (often 3 – 10%), and $15 chargeback fees for refunds or lost fraud disputes.

What’s not included: tax calculation and filing, fraud losses, and the operations, engineering, and finance time to glue it all together.

MoR costs

Blended take-rate: typically 5 – 15% of net sales (after tax).

This single fee usually covers tax calculation & remittance, chargeback handling, fraud protection, and compliance paperwork.

Why the range is wide: some MoRs absorb PSP costs inside their rate; others pass those through as line items. Always ask for an itemized quote.

Deep dive: For a detailed teardown of how MoR pricing is structured, and where hidden costs can creep in, see our full analysis here: Is your DTC Merchant of Record costing more than you think?.

Bottom line: PSPs look cheaper on the surface, but don't account for tax, fraud, and internal overhead. Plus, the potential cost that comes with all of that compliance liability. Evaluate both models with a full lens before you commit.

What a PSP does (and does not do)

PSP role | What you still own |

Routes card and alternative payments to acquiring banks and local schemes. | You are the legal “merchant” on every transaction. |

Provides PCI-DSS compliant tokenization and secure vaulting. | Collecting and remitting VAT, GST, sales tax, and digital-services levies. Updating local entity registrations and tax IDs as you enter new countries. |

Offers risk-scoring tools and basic fraud rules. | Chargeback disputes and losses. |

Gives access to dashboards, webhooks, and reconciliation files. | Compliance with PSD2, Strong Customer Authentication, and regional consumer-protection laws. |

Good fit when:

You’re striving to cut as many costs as possible regardless of required resources and liabilities.

You have resources to take on privacy, tax, and legal compliance obligations.

You already have local entities or plan to create them.

What an MoR takes off your plate

The MoR is the legal seller of record. Players buy from the MoR, not directly from your studio. That single detail shifts a long list of tasks onto their shoulders:

MoR responsibility | Result for your team |

Registers local entities, files indirect taxes, and remits funds net of tax. | Zero need to track every VAT rate or marketplace-facilitator rule. |

Handles card and alternative payments through its own PSP stack. | One integration covers dozens of markets and methods. |

Owns fraud decisions, chargeback dispute management, and fines. | Predictable cost structure without surprise arbitration fees. |

Issues receipts and complies with invoicing mandates (e.g., India GST, Brazil NF-e). | Local consumer documentation is automatic. |

Maintains licensing where payments are regulated (e.g., money-transmitter, EMI, PCI). | Faster speed to market with fewer audits or certifications. |

Good fit when:

You want to launch globally fast, without building a tax and compliance team.

You have limited resources and want to focus on new games, updates, and live ops instead of compliance.

You’re new to DTC and have limited payments and compliance expertise.

You want to leverage multiple PSPs to maximize reach and optimize performance.

Consideration to help you decide

Map your readiness. If taking on a 0.3% chargeback ratio and EU VAT filing raises red flags, then leaning on an MoR can be cheaper than hiring specialists.

Audit technical resources. Count the engineering weeks you can allocate to payments upkeep every quarter. PSP integrations are never truly “set and forget.”

Project international growth. If 80% of your 12-month plan is domestic, a PSP plus a tax-automation plug-in may be enough. If global coverage is important, MoR speed wins.

Benchmark total cost of ownership. Compare MoR’s all-in rate with “PSP gateway + acquirer fees + fraud tools + tax automation + headcount.” TCO often flips the headline price narrative.

Consider hybrid stacking. Advanced studios mix: run MoR as the fall-back for high-risk countries and use only PSP in markets where you have strong entities and have available resources.

We’re here to help

We aren’t interested in selling you one versus the other, but we can help you navigate these important decisions. Reach out for a no-strings-attached consultation via the form at the bottom of this page.